Background:

This write-up is part of what we call “Financial Wellness”. Many of us blindly pursue an investment strategy based on a family advisor or an agent who makes lot of money and provides some assistance. The framework (developed by Raj Mehta) provides insights on assessing the portfolio and identifying ways to enhance the health of the portfolio. The financial wellness is NOT financial freedom NOR it has anything to do with investment. It is about how you feel related to your finances. The details below provides you a methodology to assess your health and in the process enhance the way you feel about financial wellness (assuming the right interventions are made at the correct time)

The challenge:

- Emotions have a strong impact on Individual investors[1].

- Research has also demonstrated that individual investors demonstrate a significant preference for selling winners and holding losers[2].

Given the consistency of the returns from the equity market and the above empirical data, this study provides a framework to maintain healthy returns and processes which can sustain the results over a longer period of time.

Market Background:

The individual investor usually does not have transaction data for any analysis (except for those who work with PMS companies). A structured approach is needed to guide the individual investors in (a) doing a formal review of the progress and (b) make necessary, rational changes from time to time in their portfolio. This article provides a framework for (a).

Portfolio analysis methodology:

The review of the portfolio is based on a two phased approach. Phase I applies prioritization using Pareto Analysis followed by Phase II which maps various stocks into different quadrants for decision making.

Phase 1: Prioritization with Pareto Analysis

Pareto analysis is used across different industries as well as in finance to prioritize where to focus to achieve maximum results[3]. Based on this principle (also known as 80 for 20 i.e. 80% of the results are achieved by focusing on 20% of the causes or main factors[4]), following criteria are used to analyze overall health of the portfolio.

- Number of companies holding 80% of the investments should not be more than 15 “core” stocks. (Based on the assumptions that 15-20 stocks are sufficient for a healthy portfolio).

- Total number of companies should be <= 40. (Based on the assumption that the balance of the 20% value should be limited to few companies only, let’s call it “tail”).

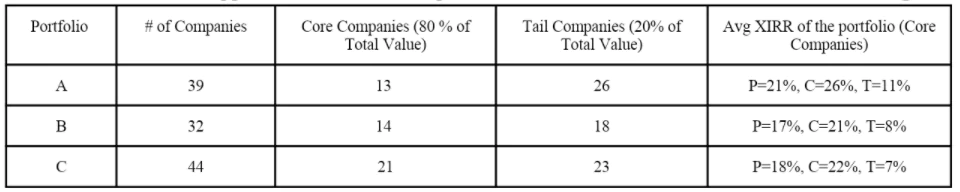

These conditions were applied to three different portfolios and the outcome is shown in Table 1 & Figure 1.

Table 1 – Overview of the portfolio elements

Applying the criteria outlined earlier, it is clear that Portfolio C needs further work. Other two portfolios may also need work on enhancing XIRR, however, it is important to prioritize a specific portfolio first. It is assumed that the value of all the portfolios is the same and hence the focus is on Portfolio C.

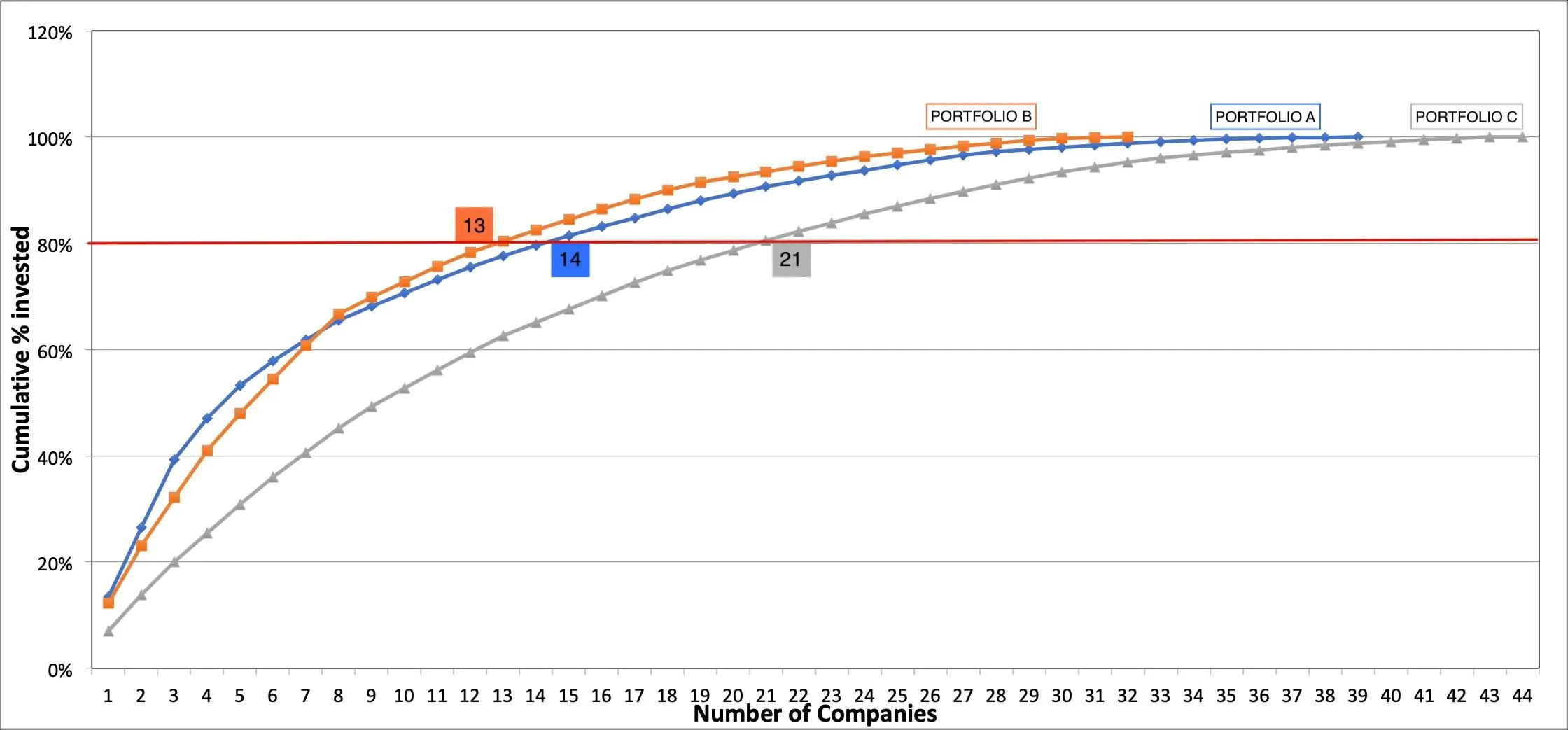

Figure 1 – Pareto analysis of 3 portfolios (X-Axis shows number of stocks and Y-Axis shows the total % of value in the portfolio).

Phase 2 – Decision making on “Core” vs “Tail” stocks.

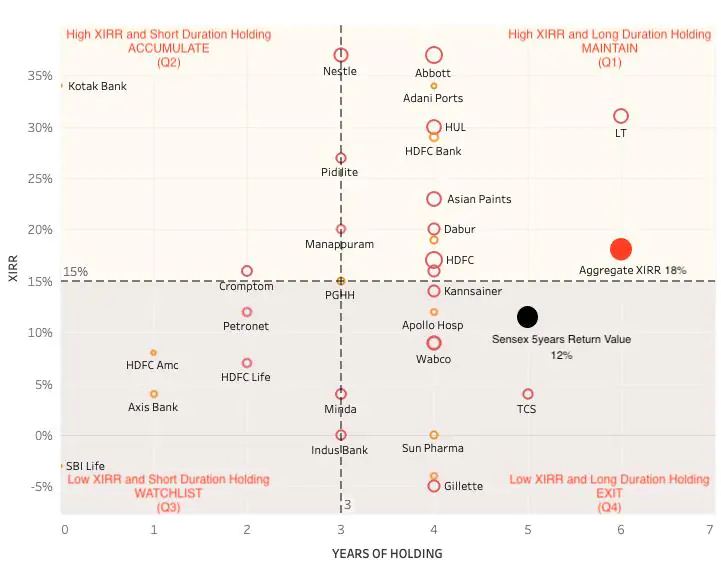

The “core” and “tail” stocks were mapped on a visual i.e. (a) Years of holding i.e. numbers of years since the first investment, on X-axis (b) XIRR on the Y-axis with shown in Figure 2 (bubble size shows % investment in each company of the total investment). In this portfolio, the number of core companies are 21 and 24 tail companies.

Figure 2 – Analysis of “Core” and “Tail” stocks. X-Axis shows Years of Holding and Y-Axis shows XIRR.

Interpretation:

Following points are highlighted using the Rule of 72[5].

- Tail Companies, i.e 23 companies in Portfolio C holding approx 20% of the investments (about Rs. 3.5 lacs) have contributed an aggregate XIRR of 7% so far. This amount would take about 10 years to double. (Table 1)

- The ore 21 companies have given a return of 22% resulting in the invested amount doubling 3+ years. (Table 1)

Recommendation:

Portfolio C owner must consider replacing the 23 “tail” stocks with “Core” stocks to achieve better returns (“Core” stocks have provided 22% XIRR as compared to Sensex returns over past 5 years of XIRR 12%). This will allow the overall portfolio to double every 3+ years as compared to 4 years as of now. It is important to realize that these numbers are based on historical data and actual data may vary. However, the recommendation is based on the need to maintain high quality stocks (similar to “Core” portfolio) to drive better than index returns, most consistently[6]. To end, we would like to emphasize that this methodology is not applicable just for financial wellness, it can be applied to most aspects of the quality of life.

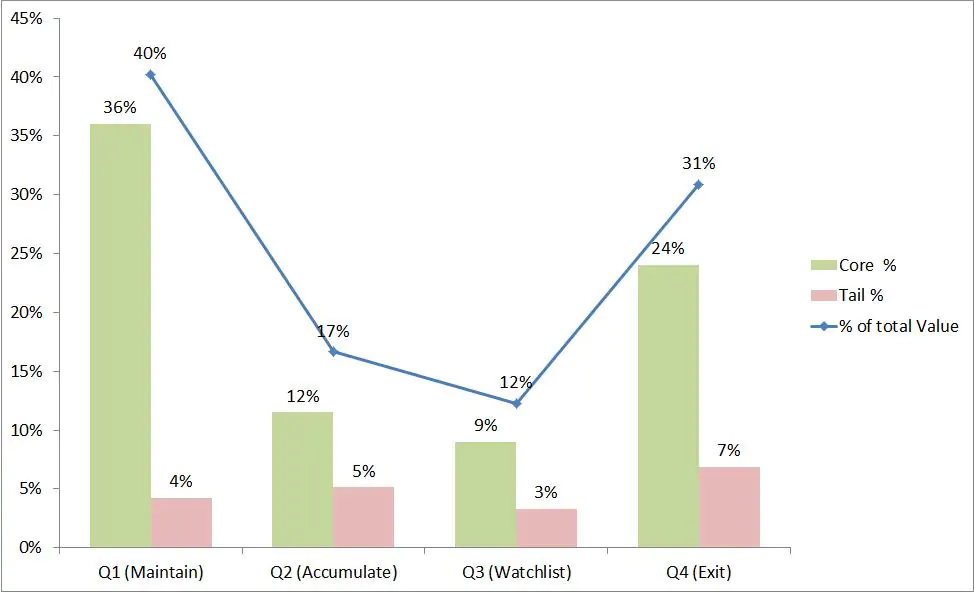

Figure 3- Quadrant-Specific data and value of “Core” and “Tail” stocks

Written by Raj Mehta and Gunjan Y Trivedi.

(Raj Mehta worked on this project during his final year Computer Engineering, Nirma University program at Society for Energy & Emotions, Wellness Space).

Additional reading: Pareto (80-20 rule) in daily life, portfolio, operations, project management, and more!

References:

[1] Dr. Sushmita Goswami, Brijesh Kishore Goswami, Dr. Aneesya Panicker, Dr. Avnish Sharma. Exploring the Role of Emotions and Psychology in Financial Investment Decisions in Indian Securities Market, International Journal of Advanced Science and TechnologyVol. 29, No. 1, (2020), pp. 532-547

[2] Odean, T. (1998), Are Investors Reluctant to Realize Their Losses?. The Journal of Finance, 53: 1775-1798. doi:10.1111/0022-1082.00072

[3] Powell, Taman & Sammut-Bonnici, Tanya. (2015). Pareto Analysis. 10.1002/9781118785317.weom120202.

[4] The 80–20 Rule of Mutual Fund Families in the U.S., K. Vaidyanathan, The Journal of Index Investing Nov 2011, 2 (3) 82-92; DOI: 10.3905/jii.2011.2.3.082 https://jii.pm-research.com/content/2/3/82

[5] Approx years to double the portfolio = (72/% Return). This provides a fairly accurate estimate of how long does it take to double the portfolio.

[6] Next article covers the process of finding stocks that are more likely to provide better than index returns, consistently.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment